Understanding the Structure of GST in India

Imagine India as a huge pizza. Every state is like a slice, and the central government is the one who baked the pizza. Now, when someone eats (consumes goods/services), both the central government and the state want their fair share of revenue.

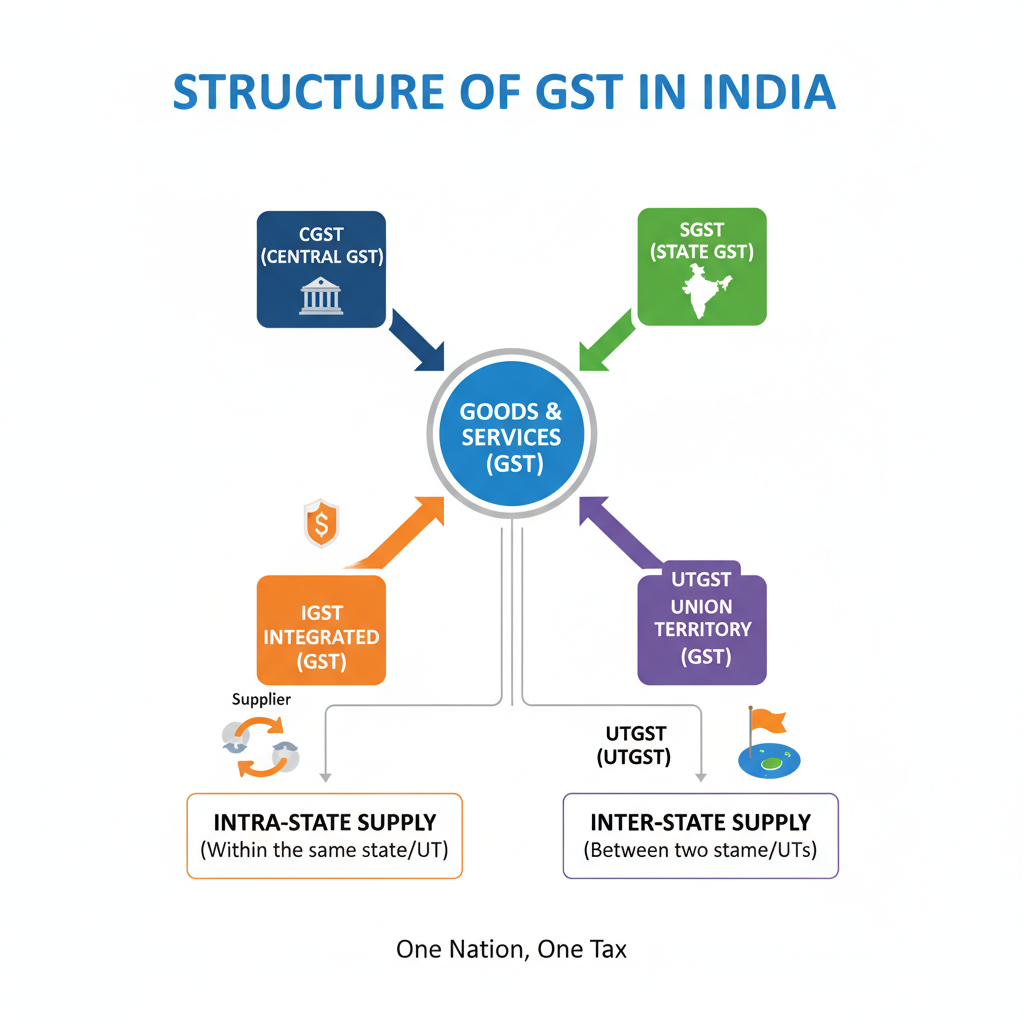

That’s exactly why GST in India follows a dual structure—the center collects its part (CGST), and the state collects its part (SGST). For goods/services crossing state borders, a special tax (IGST) kicks in.

The Dual GST Model in India

India chose a dual GST model because of its federal system. Unlike some countries (like Singapore) that have a single national GST, India wanted both the center and the states to retain taxing power.

“In simple terms, whenever GST is applied to a product or service, here’s how it gets divided:”

- The center takes its part → Central GST (CGST)

- The state/UT takes its part → State GST (SGST) or Union Territory GST (UTGST)

“This way, both the Centre and the States get their fair share of tax revenue, while people and businesses enjoy a single, uniform system across India.”

-

Components of GST

- CGST (Central Goods and Services Tax)

Collected by the Central Government. Applicable on intrastate transactions (sale within the same state).

Example: A bakery in Delhi sells a cake to a customer in Delhi. Both CGST and SGST apply. - SGST (State Goods and Services Tax)

Collected by the State Government. Also applicable on interstate transactions.

Example: For the Delhi bakery, CGST goes to the Center, and SGST goes to the Delhi Government. - IGST (Integrated Goods and Services Tax)

Collected by the Central Government. Applicable on interstate transactions (sales across state borders).

Example: The Delhi bakery sells a cake to a customer in Mumbai → IGST is charged, and later the center shares revenue with Maharashtra. - UTGST (Union Territory Goods and Services Tax)

Similar to SGST but applies in Union Territories without legislatures (like Chandigarh, Lakshadweep, and Andaman & Nicobar).

Example: A restaurant in Port Blair (Andaman) charges CGST + UTGST.

I will simply show it in a table for easy understanding:

| Type of GST | Collected By | Applicable On | Example |

| CGST (Central Goods and Services Tax) | Central Government | Intra-state transactions (within the same state) | A bakery in Delhi sells a cake to a customer in Delhi → CGST + SGST apply |

| SGST (State Goods and Services Tax) | State Government | Intra-state transactions (within the same state) | From the same Delhi bakery sale, SGST goes to the Delhi Govt, and CGST goes to the Centre. |

| IGST (Integrated Goods and Services Tax) | Central Government | Inter-state transactions (between different states) | Delhi bakery sells a cake to a customer in Mumbai → IGST charged, the center later shares with Maharashtra |

| UTGST (Union Territory Goods and Services Tax) | Union Territory Government (without legislature) | Supplies within Union Territories | A restaurant in Port Blair (Andaman) charges CGST + UTGST |

How GST Works in Real Life

Suppose we take an example:

- A manufacturer in Maharashtra makes mobile phones.

Simple memory trick: CGST + SGST = Same state IGST = Different states (or import/export) - He sells them to a distributor in Gujarat. → IGST

- The distributor sells them to a retailer in Gujarat. → CGST + SGST

- The retailer sells them to a customer in Gujarat. → CGST + SGST

This way, tax flows smoothly without double taxation.

Old vs. New Tax System

Old System (Before GST):

- Excise duty on production

- CST (Central Sales Tax) on inter-state sale

- VAT on intra-state sale

- Entry tax at state borders

New System (After GST):

- Only IGST for inter-state trade

- CGST + SGST for intra-state trade

- No entry tax or CST hassles

GST Rate Slabs—A Deeper Dive

GST is levied in slabs: 0%, 5%, 12%, 18%, and 28%. See with examples:

- 0% (Essentials) → fresh milk, rice, wheat, vegetables.

- 5% (daily use) → tea, coffee, sugar, and footwear below ₹1,000.

- 12% (standard needs) → processed food, smartphones, and packed juices.

- 18% (Common goods & services) → laptops, restaurants, movie tickets, OTT streaming.

- 28% (luxury & sin goods) → big cars, tobacco, and high-end cosmetics.

- Special rates → Gold (3%) and precious stones (0.25%).

Case Study: A Textile Shop Owner

Meet Ramesh, who owns a textile shop in Tamil Nadu.

- Sells sarees to local customers → CGST + SGST.

- Sells sarees online to Karnataka → IGST.

- Exports sarees to the USA → Zero-rated under GST.

Benefits to Ramesh:

- No cascading taxes

- Can claim Input Tax Credit (ITC)

- Easier digital filing

Destination-Based Tax

One of the biggest changes under GST is that it’s destination-based, not origin-based.

Example: A company in Punjab makes biscuits and sells them to a retailer in Delhi. Under GST, Delhi collects the tax (where consumed).

Revenue Sharing

When GST is collected:

- Intra-state supply → CGST goes to the center, SGST to the state.

- Inter-state supply (IGST) → Collected by the center, later distributed to the destination state.

Numerical Example

Suppose you buy furniture worth ₹10,000 in Karnataka. GST rate = 18% (9% CGST + 9% SGST).

- Price = ₹10,000

- CGST = ₹900 (goes to the center)

- SGST = ₹900 (goes to Karnataka Govt)

- Final Price = ₹11,800

If bought from Tamil Nadu (inter-state): IGST = ₹1,800 (collected by the center and later shared with Karnataka).

GST in Union Territories

UTs like Chandigarh, Daman & Diu, Lakshadweep, and Andaman don’t have legislatures. So instead of SGST, they levy UTGST.

Example: A hotel in Chandigarh charges CGST + UTGST.

GST and the E-Way Bill

- Mandatory for goods worth more than ₹50,000 transported across states.

- Tracks goods movement digitally.

- Prevents tax evasion.

- Simplifies logistics.

Key Benefits of GST Structure

- Uniformity—the same system across India.

- Transparency—clear breakdown of CGST, SGST, and IGST.

- Revenue fairness—destination states benefit.

- Ease for business—smooth interstate trade.

- Digital compliance – e-way bills, GST portal.

FAQs on GST Structure

Q1. Why does India have both CGST and SGST?

👉 Because India follows a federal structure, and both the center & the states need revenue.

Q2. Who gets IGST revenue?

👉 The Central Government collects IGST, then transfers a share to the destination state.

Q3. Is GST the same in all states?

👉 Yes, GST rates and laws are uniform across India, though minor exemptions exist.

Conclusion: The Backbone of GST

The structure of GST may seem complicated at first, but it’s actually logical and fair. By balancing power between the center and states, ensuring destination-based taxation, and simplifying trade across borders, GST has created a more unified Indian market.

➡️ In Part 3, we’ll cover GST Registration & Compliance—who needs to register, how to file returns, penalties, and benefits for small businesses.

Part 1 link: click here

SSC Official website: Click Here